Follow Us

Podcasts

PodcastsCatch the latest PR news & updates with PRovoke Media's PR Podcasts. Lifting the lid on key industry stories & trends, join our listeners of PR podcasts today.

Videos

VideosLatest video interviews and campaigns from PRovoke Media, previously known as the Holmes Report.

Long-form journalism that analyzes the issues, challenges and opportunities facing the business and practice of PR.

Profiles & Interviews

Profiles & InterviewsExplore PR profiles and interviews with leaders from the marketing and PR worlds.

Crisis Review

Crisis ReviewPR Crisis & Business Crisis review. PRovoke Media's annual analysis of the top reputation crises to rock the corporate sector. Read on here.

Coronavirus

CoronavirusPRovoke Media's coverage of the Covid-19 crisis, focusing on corporate communication, public affairs & PR industry fallout.

Trend Forecasts

Trend ForecastsPRovoke Media's PR Trends round up. PRovoke Media's annual forecast of PR trends and news that will impact the PR world in the year ahead...

Social & Digital

Social & DigitalDedicated to exploring the new frontiers of PR as it dives deeper into social media, content and analytics.

Technology

TechnologyOur coverage of key technology PR trends and challenges from around the world of digital communications.

Consumer

ConsumerFrom brand marketing to conscious consumerism, coverage of key marketing and PR trends worldwide.

Employee Engagement

Employee EngagementPRovoke Media's coverage, analysis and news around the rapidly-shifting area of employee engagement and internal communications.

Sports Marketing

Sports Marketing Sports PR news, diversity & inclusion trends, views and analysis from PRovoke Media. Subscribe today for the very latest in the world of sports communications.

PRovoke Media's definitive global benchmark of global PR agency size and growth.

Agencies of the Year

Agencies of the YearPRovoke Media's annual selections for PR Agencies of the Year, across all of the world's major markets.

Innovator 25

Innovator 25PRovoke Media profiles marcomms innovators from across North America, EMEA and Asia-Pac.

Creativity in PR

Creativity in PRIn-depth annual research into the PR industry's efforts to raise creative standards.

APACD/Ruder Finn annual study of Asia-Pacific in-house communications professionals.

SABRE Awards

SABRE AwardsThe world's biggest PR awards programme, dedicated to benchmarking the best PR work from across the globe.

The biggest PR conference of the year, a high-level forum designed to address the critical issues that matter most.

A global network of conferences that explore the innovation and disruption that is redefining public relations.

Agencies of the Year

Agencies of the YearUnrivalled insight into the world's best PR agencies, across specialist and geographic categories.

Our Roundtables bring together in-house comms leaders with PR firms to examine the future of communications.

Agency Playbook

Agency PlaybookThe PR industry’s most comprehensive listing of firms from every region and specialty

.jpg) All Jobs

All JobsFind the latest global PR and communications jobs from PRovoke Media. From internships to account executives or directors. See all our PR jobs here.

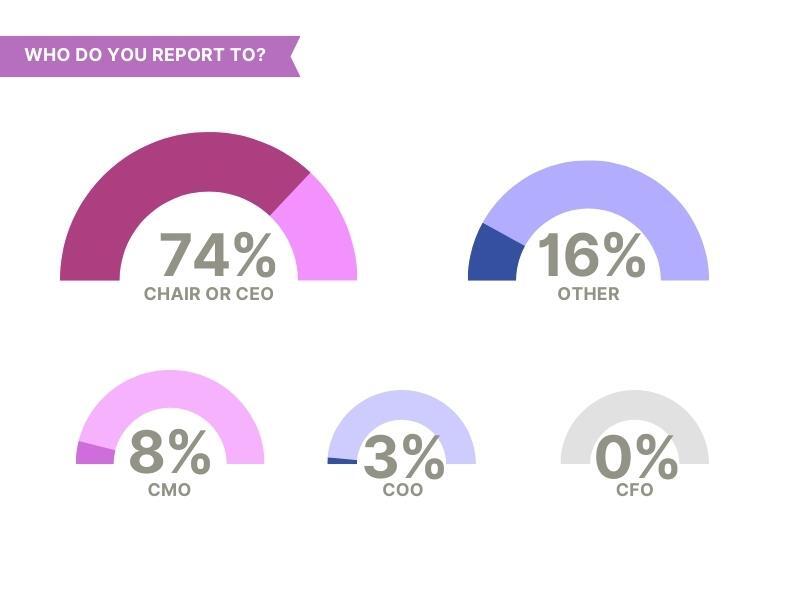

The number of CMOs and CCOs reporting to the chief executive or chair of their organization is back down to 74% this year from 81% in 2022 and 72% in 2021. Last year none of our cohort reported into the chief operations officer roles (compared to 2021, when 6% reported into the COO) and this year this is back up to 3%. As last year, none of the 100 report into the CFO. Oversight by the chief marketing officer was down from 12% to 8%. And 16% of the cohort report into other functions, such as heads of corporate relations, strategy and growth, chief impact or brand officers.

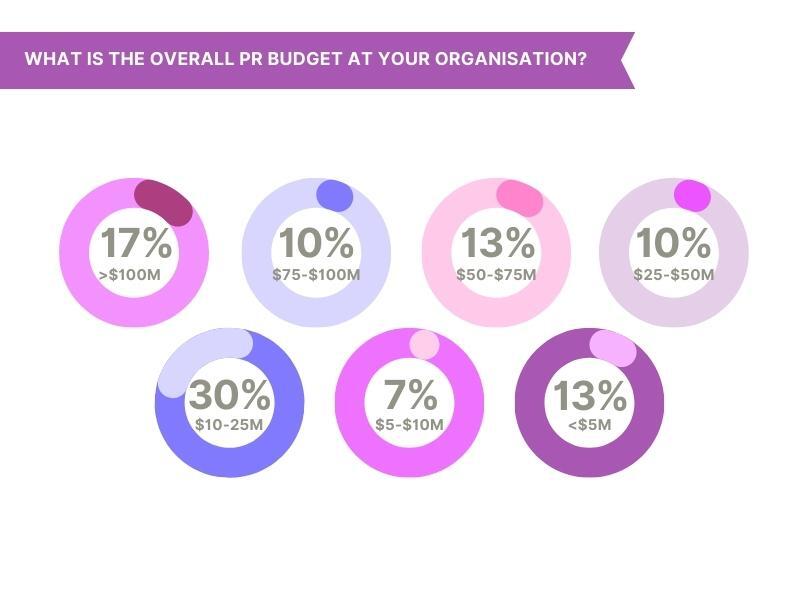

This year, an incredible $1bn has been wiped off the budgets of our Influence 100 cohort, who now control a PR spend of $3.7bn compared with $4.8bn last year and $4.7bn in 2021. This is essentially only slightly higher than the $3.3bn combined budget in 2018.

Breaking down the numbers, this is largely down to a significant dip in the number of our Influence 100 managing top-end budgets. Last year the number who managed budgets of more than $100m was 25% (compared to 27% in 2021), while this year it’s down to 17%. The number of CMOs and CCOs managing between $75 and $100m also dropped from 12.5% last year to 10% (although this is on a par with 11% in 2021), and the next budget bracket, $50-$75m, also saw a drop from 17.5% to 13%, one percentage point lower than 2021.

The number managing budgets of between $25m and $50m remained the same as last year, at 10%, and the only budget bracket that saw an increase was at the lower end, $10m-$25m, which shot up from 12.5% to 30%. At the bottom end, the percentage handling budgets under $5m was back up to 13% from 7.5% last year (in 2021 it was 14%), and those managing $5-$10m dropped from 15% to 7% (compared to 9% in 2021).

Despite the drop in combined budgets, many respondents said their own budget had remained flat this year, up from less than half last year. For the few who had seen an increase in budget, for most this was only between 5% and 10%.

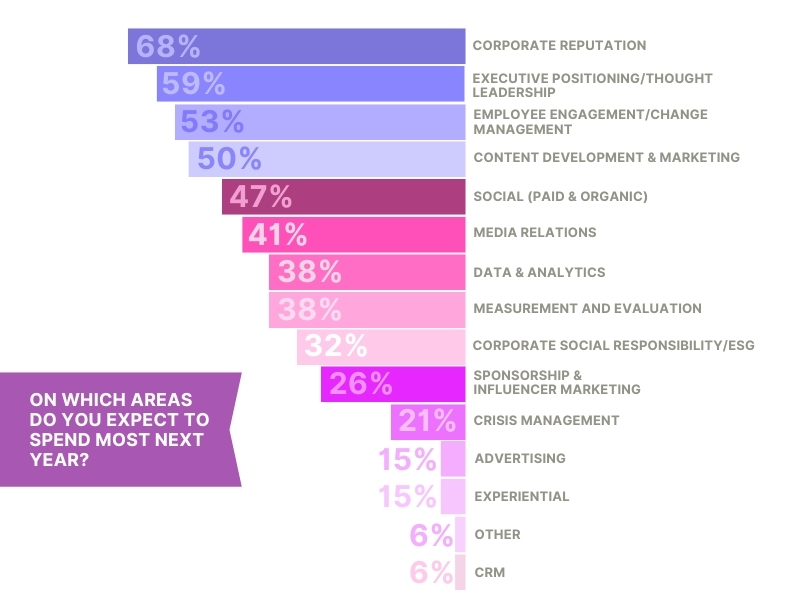

There are couple of notable changes ahead for spending priorities for our Influence 100. Corporate reputation remains the top budget priority, up two per cent from last year to 68%, but corporate social responsibility/ESG has dropped well down the table from 59% to 32%, despite the continuing focus in the industry and the wider landscape on environmental and social issues. By contrast, executive positioning and thought leadership has jumped up from 28% of last year’s Influence 100 seeing it as a spending priority, to 59%, putting it in second place. In third position as a priority area of a spend is employee engagement and change management, up from 49% to 53%. Content development and marketing has dropped slightly from being a priority for 56% last year, to 50%.

Social media has again decreased as a priority spending area, from second place on the list (60%) in 2021, to 49% last year and 47% this year. Data and analytics, and measurement and evaluation are both up slightly from 36% to 38%, while media relations is a greater priority, up from 36% seeing it as a priority area of spend, to 41%.

Other areas of note include crisis management, which after rising dramatically from 17% in 2021 to 31% last year, has settled back to being a priority for 21% of our cohort. More than a quarter (26%) see sponsorship and influencer marketing as a priority area of spend, up from 23% last year.

Advertising remains as a priority for just 15% this year (down from 23% in 2021), with experiential at the same level, and CRM is seen as slightly more important, up from 2% for the past two years to 6%, but is still bottom of the list. Other areas, such as public affairs, research and alliances/partnerships, have become less important, being seen as a priority for 6% compared to 10% last year.

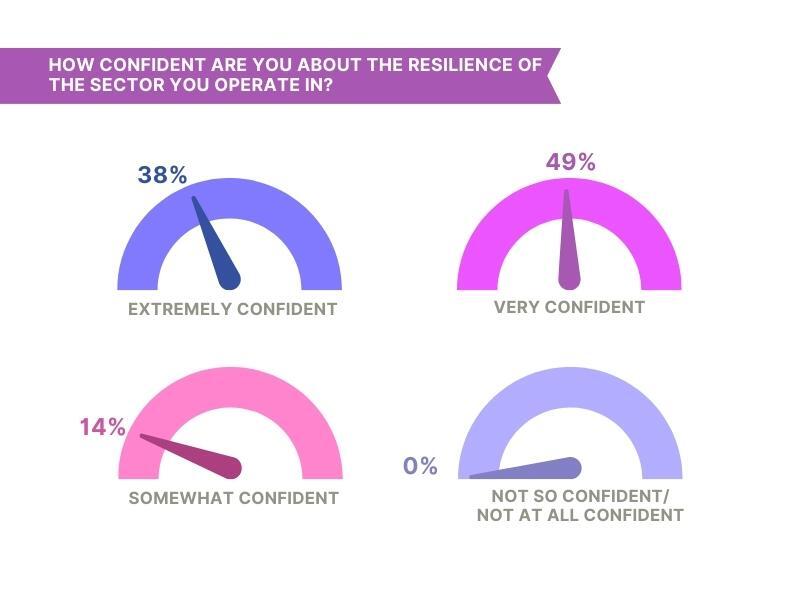

This year’s data suggests confidence in the resilience of the sector they operate has risen a little for our CCOs and CMOs, with 38% saying they feel extremely confident, up from 33.5% last year but nowhere near 51% in 2021. Those feeling very confident remained stable at 49%, as did those feeling somewhat confident, at 14%. But not one of our Influence 100 said they didn’t feel confident this year, down from 2.5% last year.

This year’s data suggests confidence in the resilience of the sector they operate has risen a little for our CCOs and CMOs, with 38% saying they feel extremely confident, up from 33.5% last year but nowhere near 51% in 2021. Those feeling very confident remained stable at 49%, as did those feeling somewhat confident, at 14%. But not one of our Influence 100 said they didn’t feel confident this year, down from 2.5% last year.

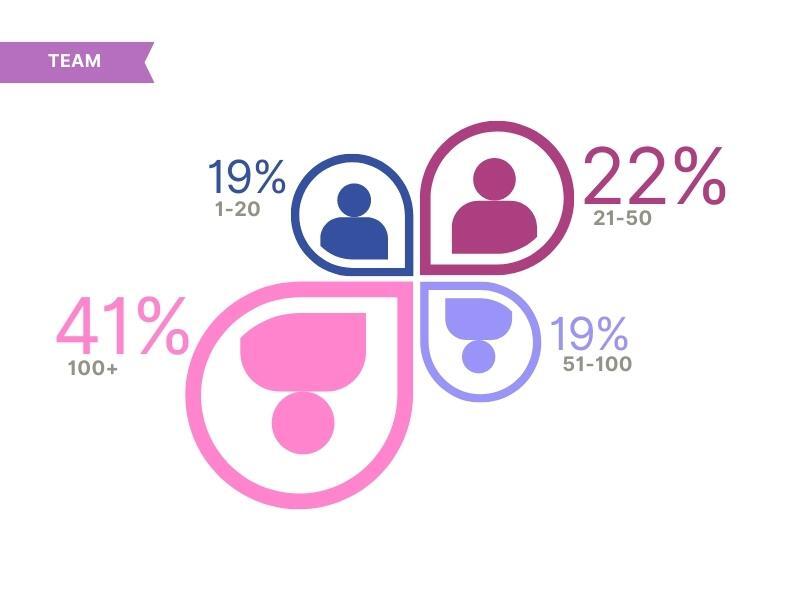

Before last year, we’d seen a steady rise in the number of our CCOs and CMOs managing teams of more than 100 people, but last year the trend stalled, decreasing slightly to 48%, and this year it’s dropped to 41%. The number managing teams from 51-100 also slipped to 19% from 21% last year and those with small teams of 1-20 almost doubled also dropped from 21% to 19%. Conversely, those managing teams of between 21 and 50 people more than doubled from 10% to 22%.

Around a third of respondents (34%) said their team had stayed the same size as last year, and a further 50% said their team size had increased by 2% and 30%, with a couple of outliers saying their team size had grown by 50% thanks to departmental mergers. A further 15% said their team had shrunk (compared to 5% last year) – by between 2% and 15%.

When asked about where they expected their teams to work, hybrid working remained the norm for the overwhelming majority – 82%, although this compares to 92% in 2021. Last year, only 7% said their teams were back in the office full time, but this rose to more than 18% this year. And while, again, none of our respondents said they had a fully remote working model, the number who said their teams were mostly remote dropped from 9% to just under 3%.

Our Influence 100 have a say over much more than just public relations – for which 100% are responsible for hiring. The majority of respondents are also the primary decision-makers for digital and social media agencies, although this is down to 58% this year, down from 71% in 2022. The number responsible for hiring advertising agencies has dropped again, from 41% in 2021, to 32% last year, and 25% this year. Other specialist agencies managed by 17% of our cohort included CRM, internal communications, investor relations, sustainability, design, content and sponsorship.

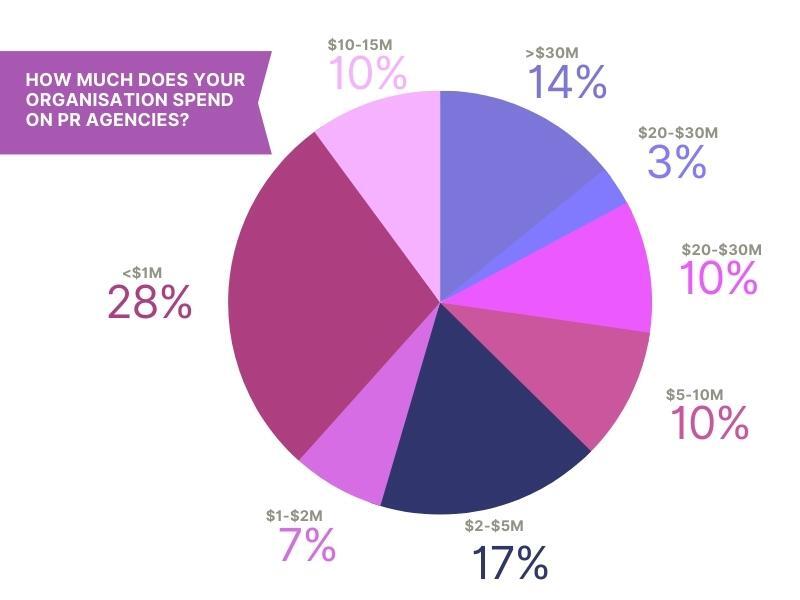

Agency spend has fallen significantly again this year. In 2021, a full 30% were spending more than $20m on their PR agency partners; last year this dropped to 26%, and this year just 17% have agency budgets of more than $20m.

A further 20% spending between $10 and $20m, compared to 25% last year. At the lower end, 28% of respondents were spending less than $1m, much higher than 18% last year. In the middle of the table, the proportions were closer to last year, although 17% were spending between $2m and $5m, up from 13% last year, and only 10% had budgets of $10-15m, down from 15% last year. Those spending between $15m and $20m and between $5m and $10m remained the same.

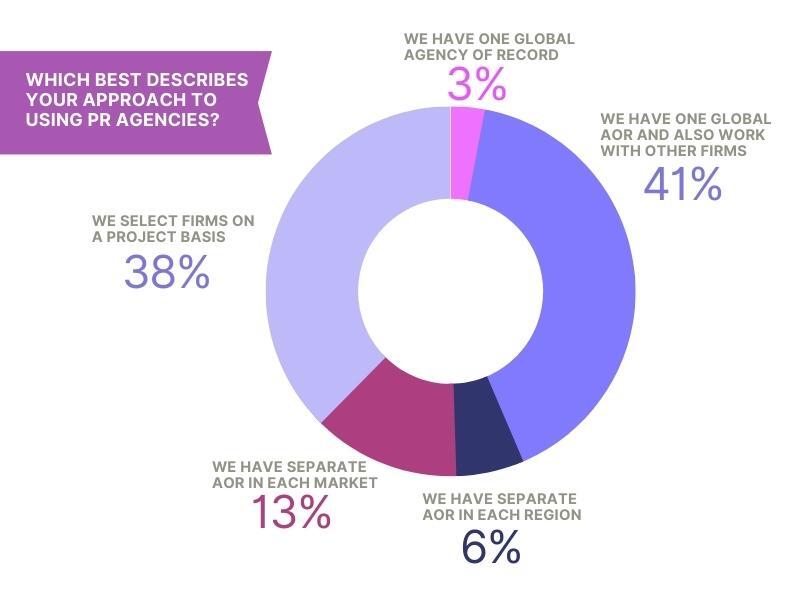

There has been another swing in the way CMOs and CCOs work with their agencies in the last 12 months, if our data is anything to go by. Just 3% say they have one global agency of record, back down to 2021’s figure of 2% from 16% last year. And the number of respondents working with firms on a project basis has risen considerably, 22% last year to 38% this year (compared to 34% in 2021).

The percentage with a global AOR who also work with other firms rose slightly to 41% compared to 36% in 2021, and the number with separate AORs in each region dropped again, from 14% in 2021, to 12% in 2022, and 6% this year. As last year, the number of CMOs and CCOs who have one global AOY and also work with other firms made up the highest proportion of the responses, at 41%, up from 36% last year.

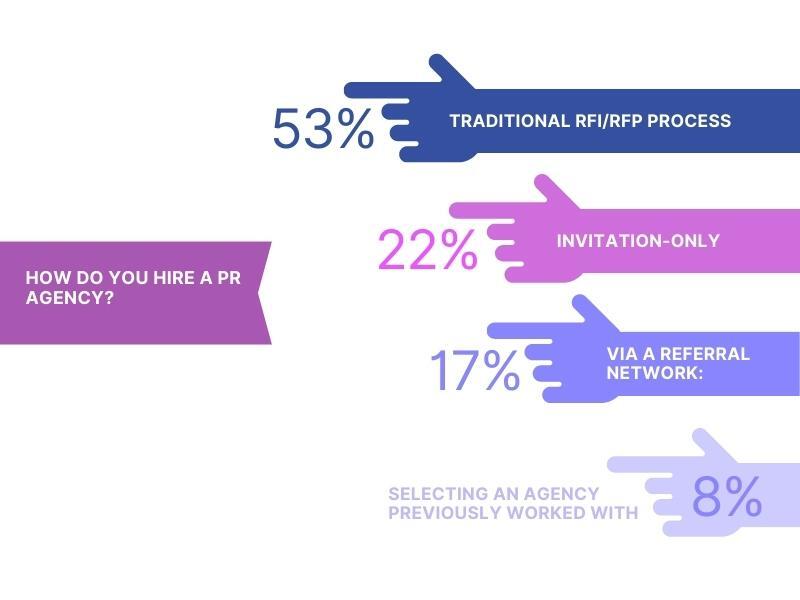

The number of CCOs and CMOs who prefer to hire agencies via a traditional RFP pitch process continued to increase, up to 53% this year compared to 47.5% last year, 45% in 2021 and 32% in 2020. Meanwhile the number who prefer an invitation-only process continued to fall, down to 22% compared to 35% last year, 39% in 2021 and a whopping 52% in 2020. The number of respondents preferring to hire an agency they’ve worked with previously rose a little to 8% from 5% last year, while those using a referral network rose from 12.5% last year to 17%.

We also asked our influencers what role procurement plays in their organization when it comes to hiring PR agencies: 81% (the same as last year) said procurement was somewhat or very involved, 14% said procurement doesn’t get involved in hiring PR agencies, down from 19% last year. Interestingly, after a few years where either none or 2% of our cohort said procurement had final sign off, this rose to 6% this year.

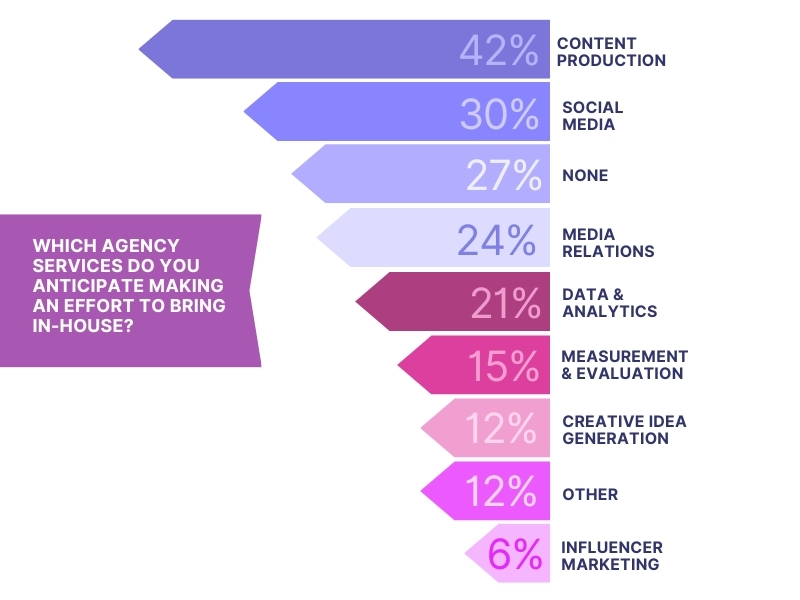

When we asked our comms leaders which services they would be looking to bring in-house, a full 42% said content production this year, up from 39% last year and 28% in 2021. Bringing social media in-house is on the agenda for 37%, the same as last year, and media relations is a priority for 24%, down from 29% in 2022.

A much smaller number are considering bringing creative idea generation in-house, down from 24% to 12%. Meanwhile, 21% are looking at bringing data and analytics in-house, down from 24% last year, and 15% said in-house measurement and evaluation was on the cards, down from 20% last year. Influencer marketing remained a less interesting option, with just 7% thinking of bringing it in-house, around the same as the 2022 survey.

In addition, a much higher number than last year are exploring bringing other areas in house (12%, up from 4%), such as sustainability communications and thought leadership. However, the number of leaders who said they wouldn’t be looking to bring any services in-house rose from 24% last year to 27%.

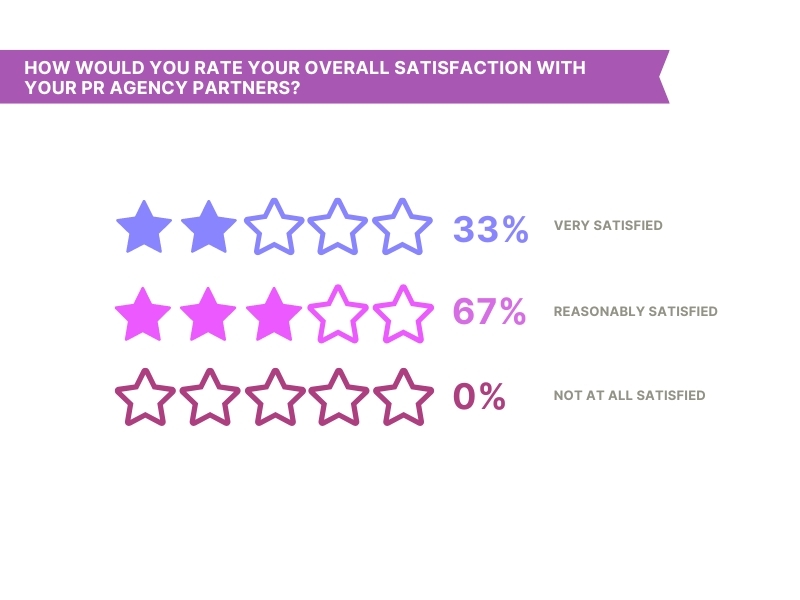

When we asked our Influence 100 how satisfied they are with their PR agency partners, the proportion that said they were very satisfied has dropped again, from 45% in 2021 to 37% in 2022, to 33% this year. There was a corresponding rise in the number who said they were reasonably satisfied, up from 61% last year to 67%. While last year 2% said they weren’t at all satisfied, this dropped to zero this year.

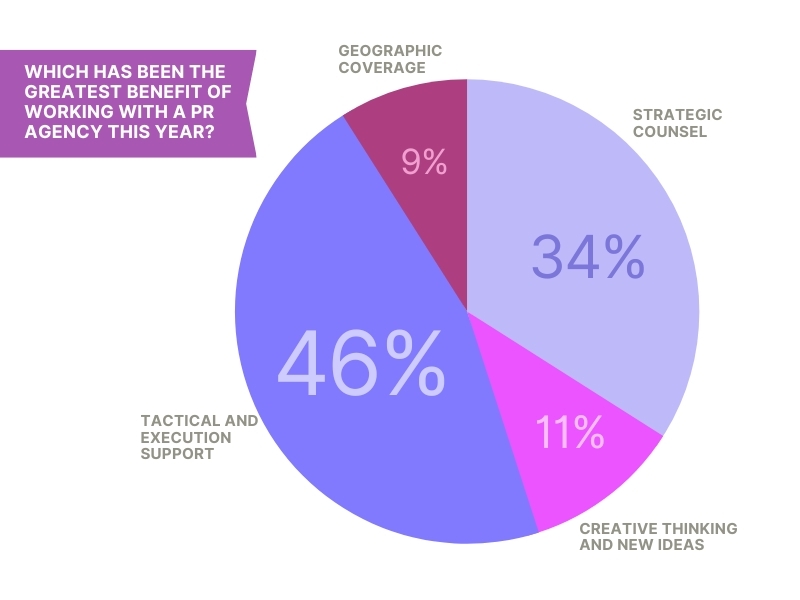

Tactical and execution support remains the biggest benefit to working with a PR agency for 46% of our influencers, up from 35% last year but down from 51% in 2021. Strategic counsel, meanwhile, was named the biggest benefit to working with a PR agency for 34% of our influencers, another jump from 30% last year and 20% in 2021. Creative thinking, however, dropped significantly as a perceived benefit, down from 27.5% to a concerning 11%; for context, in 2019, 36% of our influencers valued this above all other benefits of working with a PR agency.

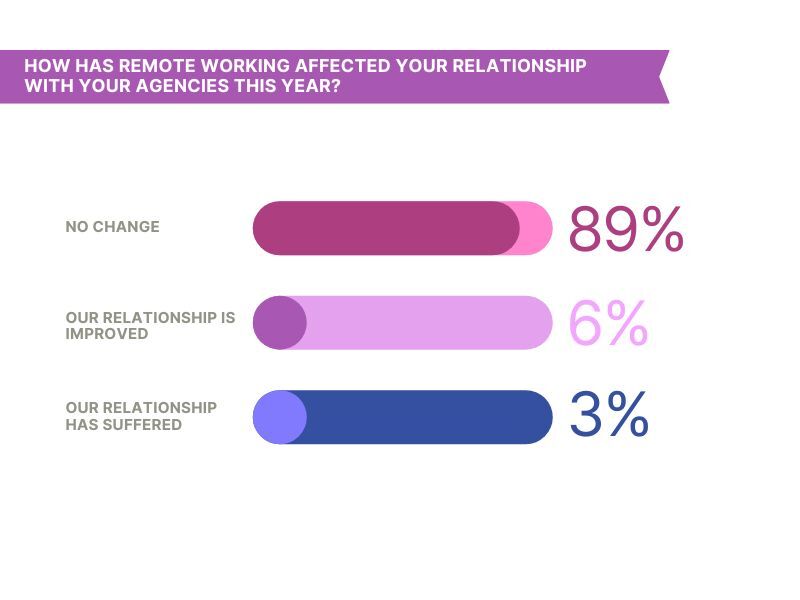

Our final question concerns how relationships with and expectations of PR agencies have changed. The proportion of influencers saying their relationship with PR agencies had suffered due to remote working dropped significant from 17% last year to just 3% this year, and the number who felt their relationship had not changed rose from 73% to 89%, both suggesting that the post-pandemic new normal is very much bedded in. Those who felt relationships had actively improved dropped a little, from 10% to 6%.

Intelligence and insight from across the PR world.

About PRovoke Media Contact Us Privacy & Cookie PolicyWe feel that the views of the reader are as important as the views of the writer. Please contact us at [email protected]

Signup For Our Newsletter Media Kits/Editorial Calendar Jobs Postings A-Z News Sitemap© Holmes Report LLC 2024